Description

This 24-page verified affidavit and framework sets out a complete legal structure for foreign fiduciary trust administration under U.S. statutory law, Treasury Regulations, and controlling Supreme Court precedent. It demonstrates how a domestic trust may file Form 1041, allocate 100% of receipts as deductible fiduciary fees, reduce taxable income to zero, and lawfully designate a foreign fiduciary.

The document details:

-

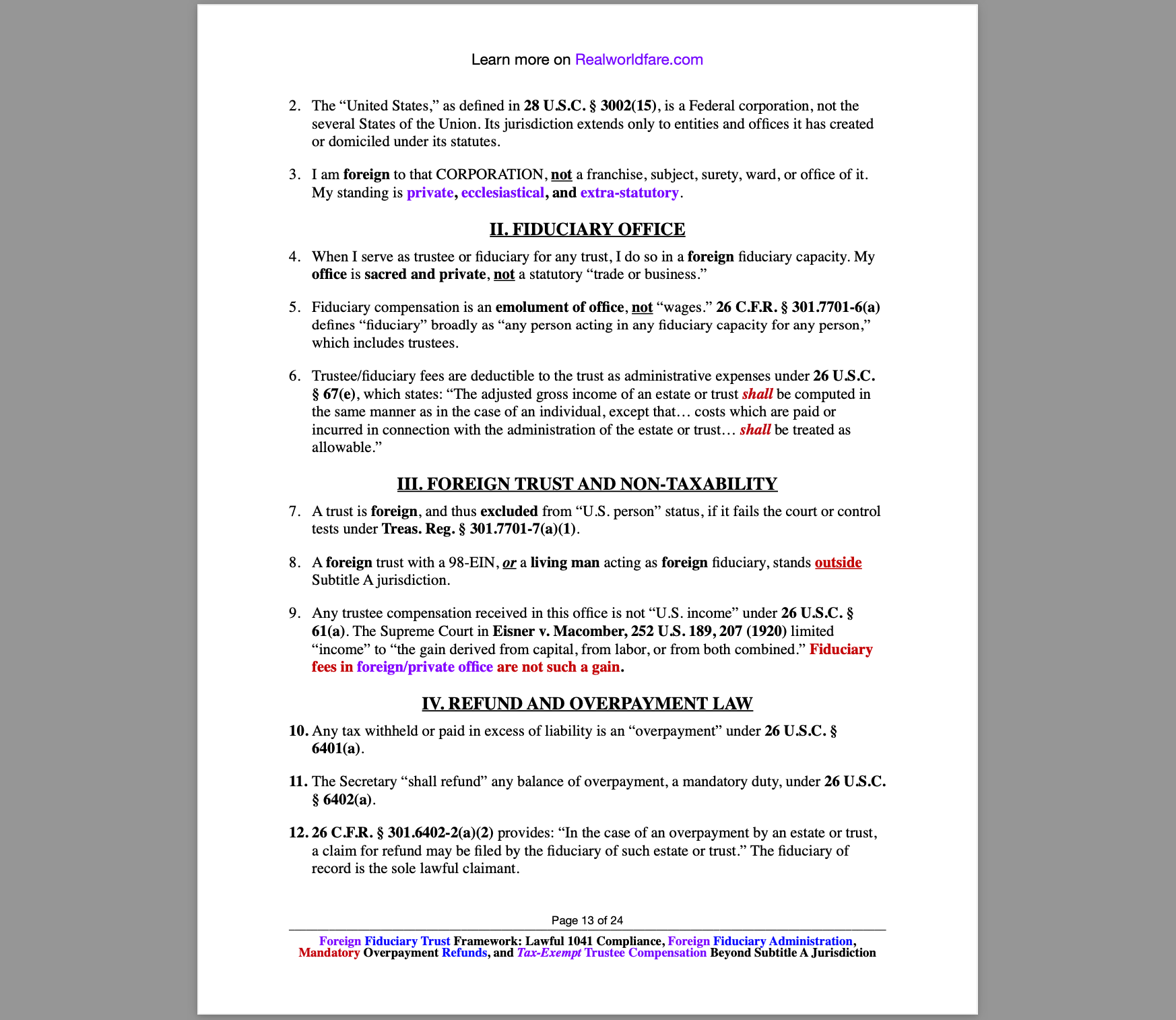

The statutory exclusion of foreign trusts from “United States person” status under 26 U.S.C. § 7701(a)(30) and Treas. Reg. § 301.7701-7.

-

The authority for trustee/administrative expense deductions under 26 U.S.C. § 67(e).

-

The fiduciary’s exclusive right to claim refunds under 26 C.F.R. § 301.6402-2(a)(2).

-

The mandatory duty of the Secretary to refund all overpayments under 26 U.S.C. §§ 6401–6402.

-

The Supreme Court’s limitation of “income” to “gain derived from capital or labor” (Eisner v. Macomber, 252 U.S. 189, 207 (1920)), excluding fiduciary compensation in foreign/private office.

It also incorporates binding maxims of law, operative effect of unrebutted affidavits, notice to agents and principals, and a formal demand for return of all overpayments, credits, refunds, and fiduciary fees.

This framework is designed as a bulletproof, affidavit-backed instrument to establish lawful non-taxability, compel refund compliance, and preserve sovereignty in trust administration.

Reviews

There are no reviews yet.