Description

UNITED STATES TREASURY INSTRUMENTS AND THE IRS TRUST SYSTEM: The Commercial Law Reality of Forms 56, 2848, 843, 1040, 1040-V, 1040-ES, 1040-NR, 1040-X, 1041, 1041-V, and 1042 — Tax Returns, Vouchers, Fiduciary Declarations, and Ledger Settlement Recorded Through the Individual Master File (IMF) and Non-Master File (NMF) Systems and Authorized by 26 U.S.C. §§ 6001 – 6065, 26 C.F.R. Part 301, and 31 C.F.R. Part 203

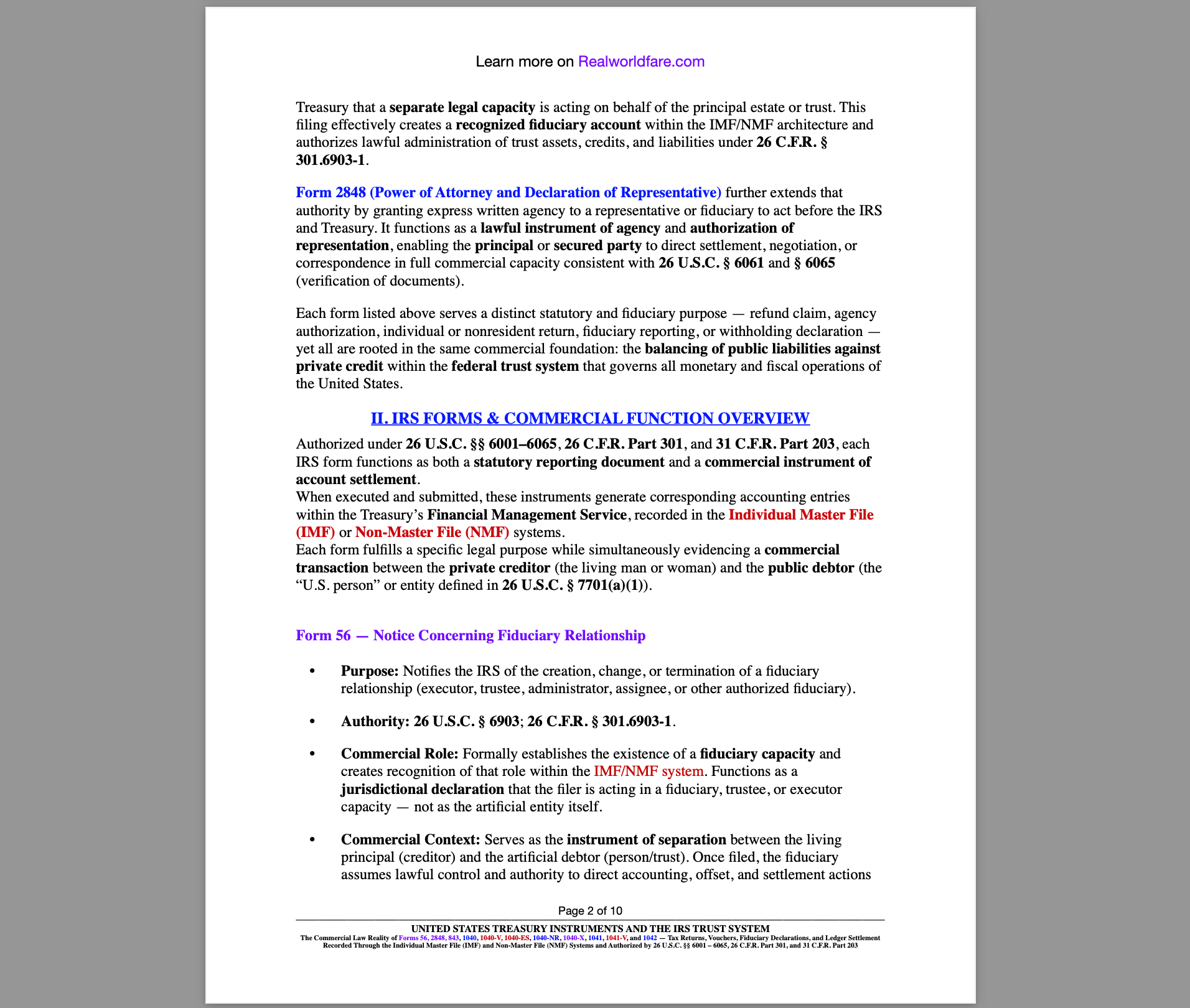

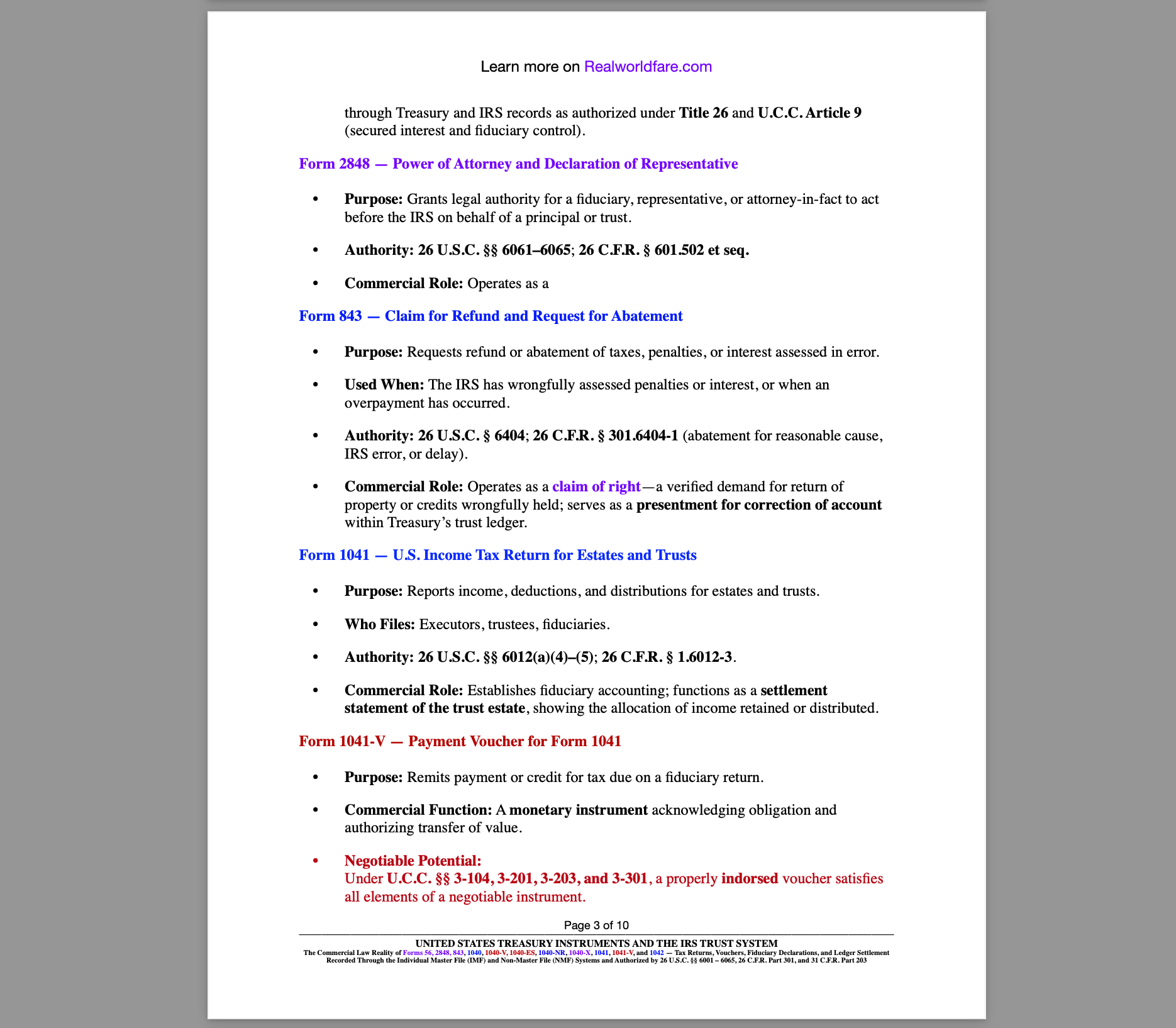

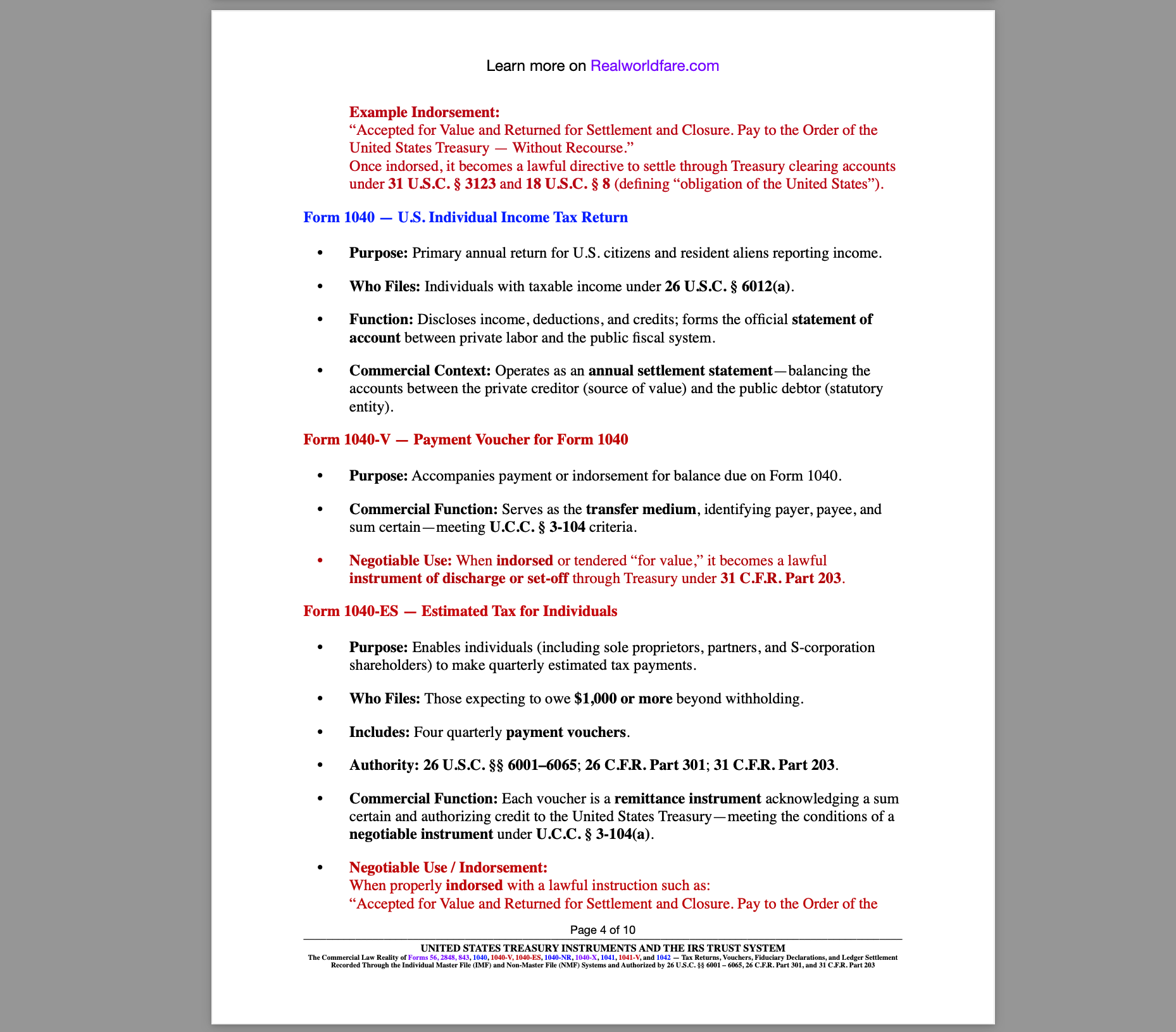

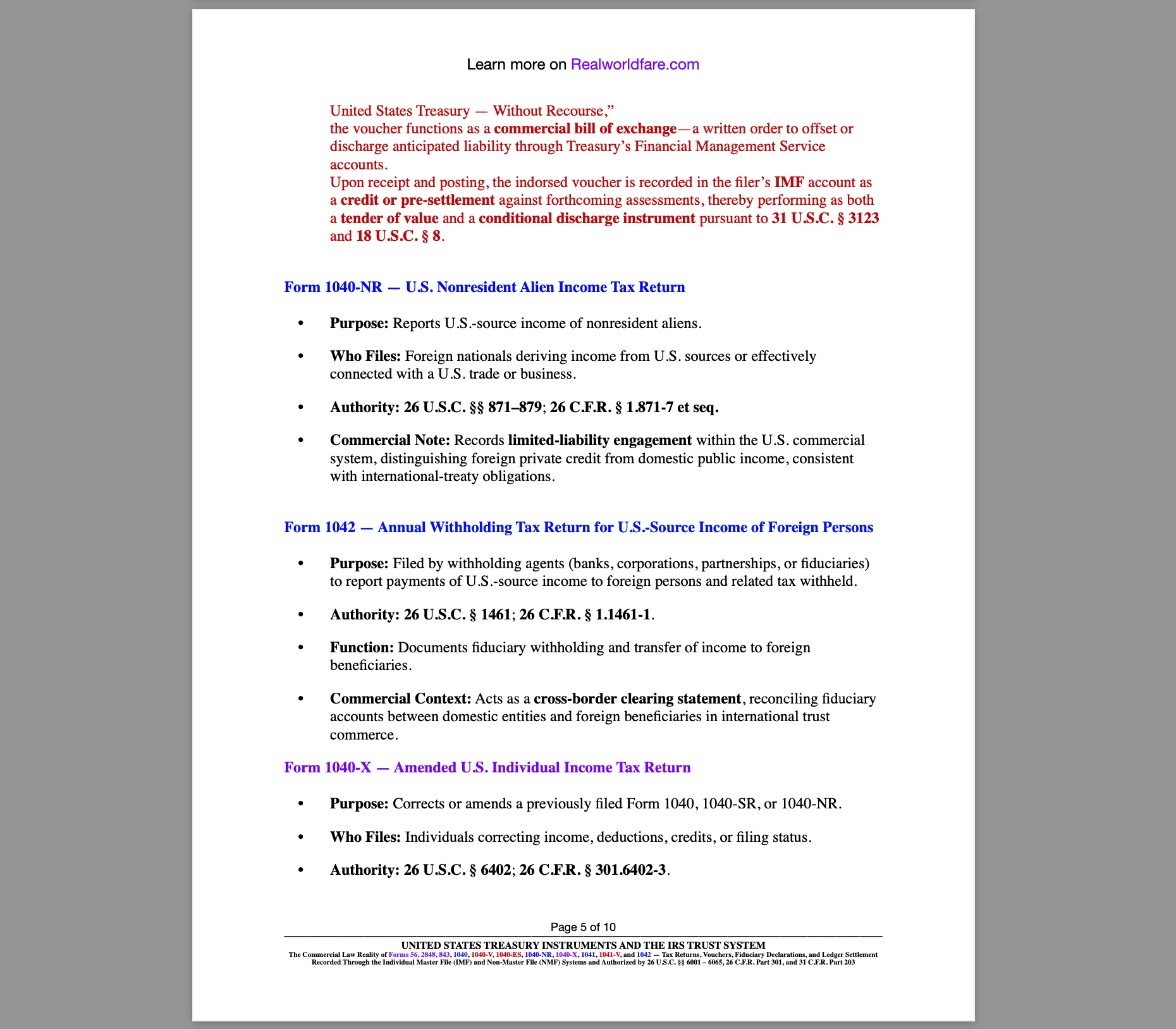

This groundbreaking document exposes the commercial and fiduciary structure behind every IRS filing — Forms 56, 2848, 843, 1040, 1040-V, 1040-ES, 1040-NR, 1040-X, 1041, 1041-V, and 1042. It reveals how these so-called “tax forms” are actually negotiable financial instruments and trust ledger events recorded through the Treasury’s Individual Master File (IMF) and Non-Master File (NMF) systems. Supported by 26 U.S.C. §§ 6001–6065, 26 C.F.R. Part 301, and 31 C.F.R. Part 203, this work lays bare the reality that the IRS is not a creditor — it is an accounting intermediary operating within a national trust and settlement system.

For those ready to move from belief to knowledge, this document delivers the lawful and commercial framework to reclaim position as creditor, fiduciary, and executor of one’s own estate.

Reviews

There are no reviews yet.