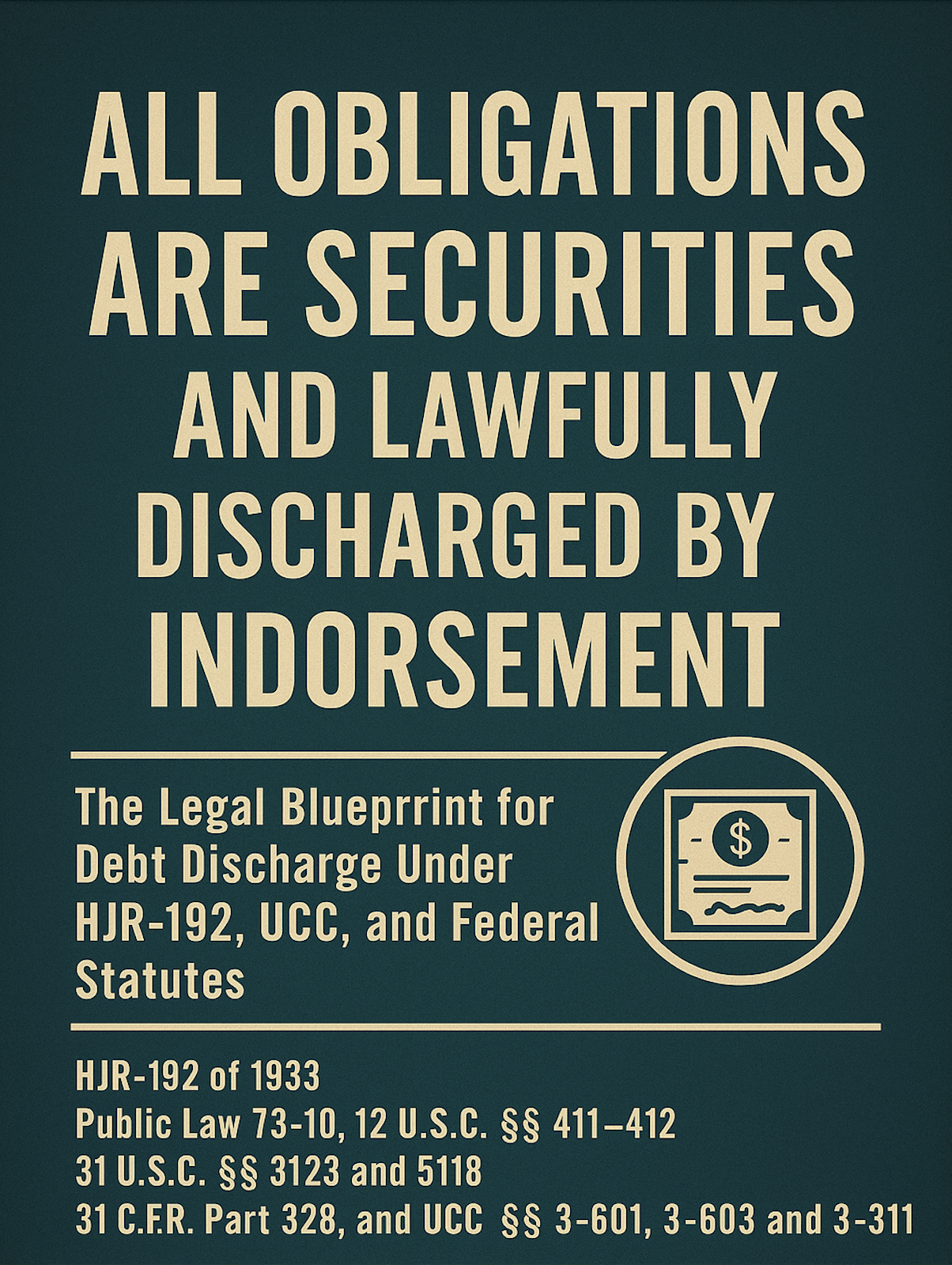

I. The 1933 Turning Point — From Gold to Credit

In 1933, the financial structure of the United States underwent a silent revolution. Congress passed House Joint Resolution 192 (Public Law 73-10), abolishing all gold clauses in contracts and declaring it against public policy for creditors to demand payment in gold. This was codified at 31 U.S.C. § 5118(d)(2), which confirms that all obligations are now dischargeable in coin or currency — not in gold or any other substance.

This marked the end of “lawful payment” in substance and the rise of discharge in credit. Since that date, no debts are truly “paid.” They are set off and discharged through credit entries within a closed commercial system.

II. All “Money” Is Debt — And All Obligations Are Securities

The statutory framework is explicit:

-

12 U.S.C. § 411 defines Federal Reserve Notes (FRNs) as obligations of the United States.

-

12 U.S.C. § 412 provides that FRNs may issue only upon collateral security, specifically U.S. obligations and other approved securities.

-

31 U.S.C. § 3123(a) pledges the full faith and credit of the United States to secure all public debt.

This means every dollar in circulation is a debt instrument backed only by collateral obligations. Citizens — through their labor, property, and commercial energy — are the pledged collateral sustaining the system.

Further, the Securities Exchange Act of 1934 and the Trust Indenture Act of 1939 classify and regulate all obligations as securities held in trust, proving that bills, statements, and notes are legally treated as securitized instruments.

III. Indorsement Is the Lawful Mechanism of Discharge

Because all obligations are securities, they are lawfully discharged the same way securities are processed — by indorsement and tender:

-

UCC § 3-601: Obligations are discharged by acts specified in Article 3.

-

UCC § 3-603: Tender of payment discharges the obligation to the extent of the tender.

-

UCC § 3-311: Tender of an instrument as full satisfaction discharges the claim when accepted.

-

31 C.F.R. §§ 328.5–328.6: Recognize and govern lawful forms of endorsement.

A properly signed or indorsed instrument — even a remittance coupon — legally constitutes tender. Once tendered, the obligation is discharged by operation of law.

IV. Fiduciary Duty and Commercial Dishonor

Banks, courts, and other institutions act as fiscal agents of the United States. They are duty-bound to process lawful tenders. Refusal or obstruction constitutes:

-

Dishonor under the UCC

-

Fraudulent conversion under the Securities Exchange Act

-

Breach of fiduciary duty under the Trust Indenture Act

-

Fraud upon the People under color of law

Any refusal to accept lawful tender is not a clerical error — it is commercial misconduct.

V. Conclusion — Enforcing Your Right of Discharge

Since 1933, all obligations have existed only as securities discharged in credit, not paid in substance. Payment is a legal fiction; discharge is the reality. Federal law, commercial codes, and trust principles confirm that a properly indorsed instrument lawfully satisfies any obligation.

Understanding this system is not a loophole — it is the foundation of the modern monetary structure. Knowing how to lawfully tender instruments and enforce discharge is essential to exercising your rights and holding financial actors to their fiduciary duties.